Transferring Mortgaged Real Estate to Your Revocable Trust

(or: why we have to ask the mortgage company for permission to transfer the rental property but not the house)

People usually establish revocable trusts to facilitate the management of their assets if they become incapacitated and to avoid probate. Those purposes are only accomplished to the extent the trusts are funded (i.e., the assets of the people making the trusts are transferred to the trusts).

Transferring mortgaged real estate to a revocable trust can be confusing, as the processes for funding depends on the type of property. Often, a funding a primary residence will involve fewer steps than funding a rental property or a timeshare. One of the reasons for the difference is the Garn-St. Germain Depository Institutions Act of 1982. The Garn-St. Germain Act made the transfer of certain mortgaged real property to trusts easier by making lender approval unnecessary for those transfers. The reason to worry about lender approval when the Garn-St. Germain Act doesn't apply is the due-on-sale clause in most mortgage documents: if you transfer property without the protection of the Act and without your lender's permission, your lender might be able to declare your mortgage amount immediately due and payable.

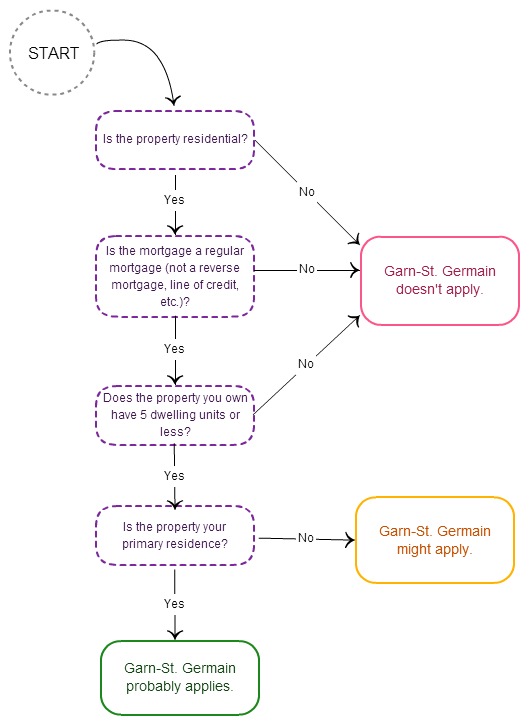

Here's a chart showing when the Garn-St. Germain Act applies:

*This chart attempts to simplify a complex law and doesn't capture all of the nuances. Consult your lawyer before transferring your property.

If Garn-St. Germain Does Not Apply...

Generally, you will need to secure the permission of the lender before transferring the relevant property to your trust. Your lawyer may recommend that you obtain a letter from the lender stating that the transfer will not trigger the due-on sale clause in your mortgage.

If Garn-St. Germain Might Apply...

Trusts and estates lawyers take different approaches in this situation. You should talk to your trusts and estates lawyer about how to proceed.

If Garn-St. Germain Probably Applies...

The Garn-St. Germain Act prevents lenders from enforcing due-on-sale clauses in the case of certain "qualifying" transfers. Your transfer might qualify for this protection, and you might not need your lender's permission before making the transfer. You should, of course, consult with your attorney to verify that before making any transfers.

Even if the transfer of your home qualifies for the protections of the Garn-St. Germain Act, your loan documents might require you to notify the lender in case of any transfer. The notification can often be done by letter after the transfer.

Conclusion

If the Garn-St. Germain Act applies to a transfer, the transfer can often be made without obtaining the permission of the mortgage lender in advance. This makes the transfer process a little bit easier, as no one has to write to the lender, jump through the hoops of the lender's choosing, and wait for a written response from the lender. If the Garn-St. Germain Act does not apply to a transfer, lender permission is generally required. Some lenders are quick to grant permission, while others are not. Lenders are not required to grant permission for a transfer to a revocable trust at all, though many seem generally willing to grant permission.